Mobile Wallet Trends in South Africa: What’s Next for 2026?

November 28, 2025

Automating Recurring Billing with Netcash (2025 Guide)

December 12, 2025Disclaimer:

This blog offers general guidance based on information available at the time of publication. For the most up-to-date details, please contact Netcash or other service providers directly.

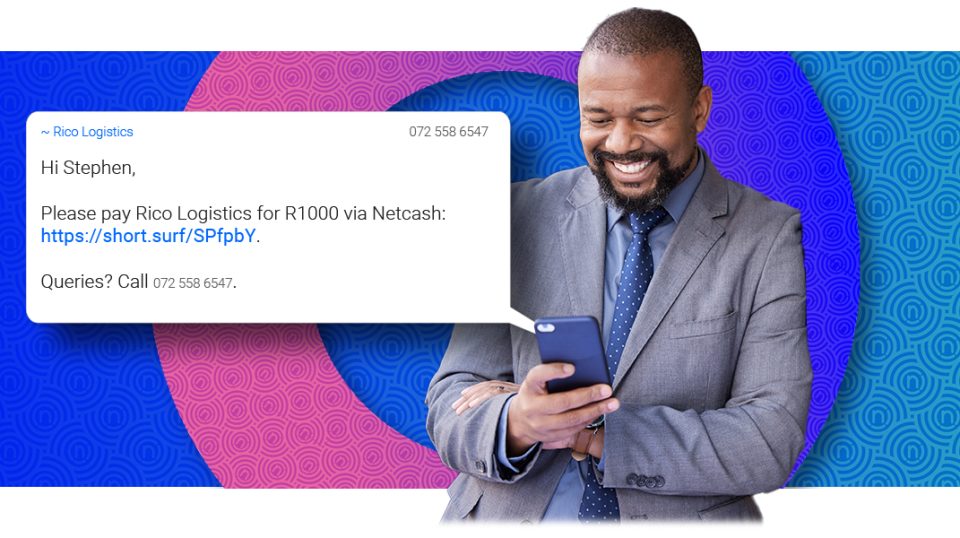

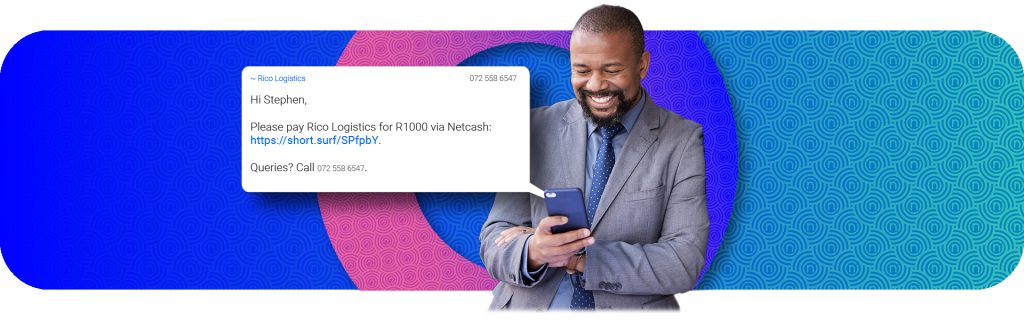

It’s no secret that many South African businesses rely on debit orders to collect recurring payments securely and consistently. To put that in context, the PASA 2023 Integrated Report states that there were 443 million EFT debit transactions and 180 million DebiCheck transactions in just one year.

So, whether you’re managing subscriptions, memberships, or monthly service fees, debit orders can help your business have consistent cash flow and reduce admin for your staff. But, there’s a catch. Not all debit order systems are created equal. Understanding the difference between DebiCheck and Registered Mandate is becoming one of the most searched-for debit order topics in South Africa. That’s where this detailed guide comes in.

DebiCheck and Registered Mandate are the most commonly used options for monthly payment collections. But which one should you choose for your business? This guide unpacks all you need to know about these methods, their cut-offs, tracking, disputes, reversals, and more.

Take the guesswork out of debit orders.

Let Netcash help you choose — and run — the right collection method for your business.

Overview of DebiCheck vs Registered Mandate in South Africa

South Africa’s debit order rules have changed significantly since the introduction of DebiCheck. Many businesses still aren’t sure when to use DebiCheck or when a Registered Mandate is appropriate, especially as RMS has now been phased out. This guide helps you choose the correct payment collection method.

Over the last few years, the South African payments landscape has undergone significant changes. In an effort to modernise and enhance security and efficiency, the South African Reserve Bank (SARB) introduced DebiCheck to protect both businesses and their customers.

They also replaced the Registered Mandate Service (RMS) with Registered Mandate (RM). While both options help businesses collect payments electronically, they operate under different rules, carry different risks, and offer varying levels of customer protection and authentication.

Let’s take a closer look at the core differences between DebiCheck and Registered Mandate.

What is DebiCheck?

DebiCheck is South Africa’s authenticated debit order system, introduced by PASA and the South African Reserve Bank (SARB) to reduce debit order fraud and disputes. The system requires account holders to electronically confirm debit order mandates with their bank. It is a once-off confirmation that typically occurs at the beginning of any contract or agreement.

This means that the customer’s bank knows the details of the agreement and will not allow the DebiCheck to be processed outside these terms. This authentication step is what makes DebiCheck the most secure debit order method available in South Africa today. For businesses, this reduces the risk of debit order disputes and complaints, enhancing cash flow and lowering admin costs and penalty fees.

How does DebiCheck work?

Here’s how the process typically unfolds:

- DebiCheck mandate creation: Your business (via Netcash or another service provider) submits a mandate request to the customer’s bank.

- Customer authentication: The customer receives a prompt from their bank through their mobile app, SMS, or internet banking to confirm or reject the debit order.

- Mandate storage: Once confirmed, the approved mandate details (amount, frequency, and collection dates) are stored securely at the bank.

- Payment collection: Your business can then collect funds based on the approved mandate without needing to reconfirm each debit.

- Tracking and cut-offs: DebiCheck collections can be tracked for up to 10 days, depending on the payment stream (AC or RM), to ensure successful payment.

What is a Registered Mandate?

A Registered Mandate (RM) is a formally registered debit order agreement—electronic or paper—that allows a business to debit a customer’s bank account without requiring DebiCheck authentication. The South African Reserve Bank stipulated that the Registered Mandate would replace the Registered Mandate Service (RMS) as of May 12, 2025, after which RMS transactions will no longer be accepted.

The Registered Mandate forms part of the broader DebiCheck framework, working as a system for processing agreements that were not authenticated. This makes RM essential for transitioning older mandates, legacy customers, or cases where authentication is not feasible. Like the RMS, this new system acts as a safety net. By allowing payment collection for mandates without authentication, the system safeguards service providers against payment delays that could disrupt their cash flow.

That said, a Registered Mandate does not mean there is no oversight on unauthorised debit orders. The customer’s bank will still capture the details of the agreement and notify the account holder about the mandate, sharing the service provider’s information and the contract reference.

A note on Registered Mandate (RM) vs Registered Mandate Service (RMS)

The RMS was a temporary system introduced by the South African Reserve Bank to process unauthenticated debit orders during the new DebiCheck system rollout. It served as a fallback for businesses and customers to manage collections during the transition to DebiCheck.

This time also allowed the Payments Association of South Africa (PASA) to educate people on how the new system is more secure, efficient, and protects both businesses and consumers.

RM replaced RMS, but the two are not entirely the same. Have a look at the table below to see some of the key differences and similarities between the old RMS and the new RM systems.

| Feature | Registered Mandate Service (RMS) | Registered Mandate (RM) |

| Status | Temporary solution, now phased out | Official payment rail, successor to RMS |

| Authentication | Used when the customer failed to authenticate a debit order | Can be registered without a failed or expired authentication |

| Processing Time | Early morning collections after DebiCheck | Evening collections, with tracking from midday to midnight |

| Customer Tracking | Limited visibility | Allows customers to track their payment obligations for up to 10 days |

| Disputability | Yes | Yes |

How does Registered Mandate work?

Here’s how the Registered Mandate initiation usually goes:

- Mandate setup: A Registered Mandate (RM) can be created in two ways: (1) when a customer does not authenticate a DebiCheck mandate within the stipulated time, or (2) your business requests the registration of the mandate against a customer’s account.

- Customer notification: The customer’s bank notifies them that an RM has been registered on their account, and shares the business’s details and contract terms.

- Payment collection: You initiate recurring debit orders based on the agreed terms.

- Tracking: Allows customer account tracking for up to 10 days after the initial action date.

- Customer rights: The customer can suspend the RM and prevent future collections, and can also amend or cancel it, depending on their bank’s functionality.

Ready to reduce reversals and protect your cash flow?

Move your debit orders to Netcash for secure, verified DebiCheck collections.

Comparison table: DebiCheck vs Registered Mandate

Smooth and secure debit order collections are a fundamental part of running a monthly payment-based business. Let’s take a look at the difference between DebiCheck and Registered Mandate, so you can make the right choice for your business operations.

| Feature | DebiCheck | Registered Mandate (RM) |

| Authentication | Customer approves the mandate electronically (via banking app or SMS) through their bank before the first debit | Does not require customer authentication; the bank notifies the customer about the RM |

| Oversight | Bank-verified; the customer must actively confirm | Bank notified of mandate; account holder receives confirmation and service provider details |

| Implementation Speed | Slightly slower, as it depends on the customer’s bank authentication | Faster; can proceed once the customer signs or agrees to the mandate |

| Dispute Risk | Very low; only unauthorised or mismatched debits can be reversed | Moderate; disputes allowed within standard debit order rules |

| Security | High; customer authentication reduces the risk of fraud | Moderate; the bank is notified and must share details with the customer and await their approval |

| Tracking Window | 10 days | 10 days |

| Best For | High-value or long-term contracts (insurance, finance, education) | Smaller or lower-risk recurring payments (subscriptions, memberships) |

| Use Cases | Insurance, loans, education, telecoms | Gyms, rentals, digital services |

Cut-off and tracking rules

When managing debit orders, timing is everything. Understanding the cut-off and tracking rules of your payment collection system helps ensure your collections go through successfully. These rules are especially important for businesses running subscriptions, memberships, instalment plans or recurring monthly services.

DebiCheck

- Action date: The specific date the debit is scheduled for processing.

- Cut-off times: DebiCheck collections must be submitted one business day before the action date.

- DebiCheck tracking window: You can track unsuccessful payments for up to 10 consecutive days.

- Mandate validity: Remains active as long as the terms are unchanged (amount, frequency, account).

- Late tracking: If payment fails on day one, the system automatically retries during the tracking window until the payment is successful.

Registered Mandate

- Action date: The date a debit order collection is submitted for processing.

- Cut-off times: Vary by bank; for example, FNB's cut-off for submitting collections is from 08:00 to 11:45 on business days.

- Tracking: Up to 10 days after the initial action date

- Mandate expiry: The mandate remains active for as long as the contract is valid.

- Resubmissions: You can re-present failed transactions within the tracking period without requiring re-authorisation.

Frequently Asked Questions

Choosing the right option for your business

Both DebiCheck and Registered Mandate have an important role to play.

If your business needs secure, customer-verified transactions, particularly for recurring services like insurance premiums, loan repayments, or subscriptions, DebiCheck is the best choice. It builds trust, reduces reversals, and keeps you fully compliant with banking regulations.

If you’re transitioning from RMS or managing older mandates that haven’t yet been authenticated, the RM helps ensure continuity without interrupting your collections. It’s a reliable fallback that supports smoother cash flow as you move towards full DebiCheck adoption.

Worried about payroll errors slipping through?

Count on Netcash for accuracy – Our platform minimises mistakes,

ensuring each employee receives the correct amount, every time.

Author:

Johann Bensch

Product Owner • Technical

Stay in Touch![]()

![]()

![]()

![]()

Johann is a globe-trotting banking guru with a serious soft spot for making things better (and building cool stuff!). He's all about taking an idea from "aha!" to "amazing!", leading tech teams, and playing well with others (engineers, designers, bosses – the whole gang!). If there's a knotty problem, Johann's your guy – he untangles it with tech smarts and always aims for a win-win for everyone, especially the clients. Plus, he's got a knack for turning big business goals into reality.

{kind=link}

{kind=link}

{kind=link}

{kind=link}