WooCommerce vs. Shopify – Which one should you choose?

April 25, 2025

WooCommerce vs Netcash Shop: Which eCommerce Platform is Right for You?

May 9, 2025Debit orders have long been and continue to be a widely used and exceptionally efficient payment collection method for millions of South African businesses. Although various direct debit systems exist worldwide, not all are created equal.

Putting a uniquely local spin on the concept, the ins and outs of SA’s homegrown debit order system make it an attractive payment collection solution.

Debit orders are a necessity for businesses looking for a cost-effective way to receive payments that is adaptable to various payment structures and easily automated. Facilitating seamless, innovative, and user-friendly debit order collections, Netcash does debit orders the right way.

Take the admin out of your collections

Chat to us about the best options for your business, or register for your account today.

TLDR: Debit orders

In a nutshell, debit orders are a type of “set-it-and-forget-it” payment and collections service. Businesses utilise this method of collecting funds thanks to its convenience and user-friendly experience, reducing human error while benefiting consistent, assured cash flow. On the other hand, individuals prefer debit orders for simplistic automation of recurring payments for regular bills and accounts.

What is a debit order?

So, what is a debit order anyway? Without getting overly technical, think of it as a once-off permission slip (called a mandate) given to a third party, authorising them to withdraw a set amount from a bank account regularly.

Debit orders are ideal for companies running subscription-based services, collecting loan repayments, or providing monthly services. They remove the need for manual intervention.

But why the need for debit orders in the first place? It all comes down to their automation. After a debit order mandate is in place, the guesswork around payment collection is eliminated. There is no more chasing customers for payments or sending out numerous payment requests. Thanks to automated debit orders, businesses reduce their administrative burden, decrease potential late fees, and keep cash flow steady and reliable.

What is an example of a debit order?

Before diving into debit order examples, it’s vital to know that South Africa has several types from which businesses can choose. Which ones work best depends on business-specific needs, yet they share many of the same traits.

- Standard debit orders (Electronic funds transfer): This type is the most common and straightforward. It involves an individual authorising a business to collect an agreed-upon amount on a specific day each month.

Example: A monthly subscription-based service or product, insurance premiums, or monthly memberships.

- DebiCheck debit orders: Essentially replacing Authenticated Early Debit Orders (AEDOs) and Non-authenticated Early Debit Orders (NAEDOs), DebiCheck requires an individual’s real-time electronic confirmation before the first debit order is processed. This acts as a signed mandate, and the debit order will be processed on the same day each month for the agreed-upon amount.

What is the difference between a debit order and a stop order ?

As diverse as the financial landscape is, the debit order ecosystem is equally as expansive and unique. Why is that important to know? Well, enter stop orders – debit order’s sibling. Wait, what is a stop order? Playing a valuable role in payment collections and scheduling, here’s what you should know.

- Debit orders: An agreement between an individual and a third party authorising the third party to deduct funds from the individual's bank account.

- Stop orders: An agreement between an individual and their bank permitting the respective bank to make a series of future-dated recurring payments to a third party.

Alongside the above, remember that a stop order can be cancelled at any stage. A debit order can only be cancelled if it is no longer valid and only upon direct request to the respective bank.

Do banks charge for debit orders?

Yes, there are standard processing fees applicable to each debit order. However, they differ from one bank to the next and are easily found within the institution's fee structure.

Note: The amount charged may be fixed or can vary depending on service agreement terms.

What happens if you don't pay a debit order?

Unfortunately, unpaid debit orders are common in South Africa, with PASA (Payments Association of South Africa) estimating that 1.2 million of 31 million debit orders go unpaid each month.

Beyond the blow to the economy, what happens to individuals who fail to meet their debit order commitments?

When someone misses a debit order payment due to a lack of available funds, it signals to credit bureaus and lenders that you might be in a financially tough spot. That alone is enough reason for these and other institutions, like banks, to assume that you could miss future payments, as your credit record is directly linked to debit order payments.

Note: Banks have different terms and conditions regarding unpaid debit orders but may charge penalty fees or late payment fees, known as a “dishonour fee,” if a debit order is returned due to insufficient funds.

For businesses, this also has potentially severe consequences that could negatively impact cash flow, increasing the need for a secure and safe system of unpaid debit order management.

note for upload: link to article of same name

Streamline the collection of debit orders from your clients

Chat to us about your Debit Order needs or apply for your account now.

Can a bank in South Africa take money from an account without permission?

Many people have questions about the possibility and legality of a bank deducting money from their current account without their knowledge or permission to settle an unpaid debt.

Until recently, banks have argued that they are allowed to do so under the common law “set-off” principle. Affirming their argument that being able to do so also provides them more peace of mind in handling payments on behalf of individuals.

However, things have changed with the enactment of the National Credit Act (NCA). The High Court decided in National Credit Regulator v Standard Bank of South Africa Limited that a bank cannot apply the common law set-off principle if the NCA applies to your agreement.

Banks and other financial institutions or credit lenders must get express permission from an individual before taking money out of one account to cover debts in another.

Debit order payments through Netcash

Netcash is the ideal Payment Service Provider (PSP) for simplifying your recurring payments and boosting cash flow with our industry-leading collections service. We manage your debit order process and offer flexible collection services, E-mandate solutions, extensive payment reporting, and effortless integration.

Debit Order Use Cases

Debit orders have become such an assumed part of daily life that it can sometimes be challenging to decide when to agree to one or when to decline. Like most things, there are better times to use a debit order to make or collect payments.

When are debit orders a good choice?

First, let’s discuss when you should consider a debit order. Businesses that operate on the foundation of recurring payments benefit most from an effective debit order collection and processing system.

Debit orders assure payment and flexible deduction schedules, making them perfect for individuals who don’t want to worry about payments and companies that rely on a timely cash influx.

Wait. What is a recurring payment?

A recurring payment is exactly that. It’s a payment method that allows businesses and service providers to collect money from a customer’s account at predetermined intervals. Keep in mind there are two types of recurring payments:

- Fixed: Individuals are charged the same amount on the same day each month unless there has been a notified price increase. (E.g. a monthly Spotify subscription billing).

- Flexible: Individuals are charged an amount corresponding to how much of a specific service said individual has used over an agreed-upon time. (E.g. a pay-as-you-go internet service provider fee).

So, what do ideal debit orders look like? These can vary, but typically, the best use cases for debit orders are:

- Regular payments made to membership organisations. Think gym memberships, insurance premiums, streaming subscriptions, and everything in between.

- Services that do not require immediate payment and function on invoicing, such as consulting firms, internet service providers, and agencies.

- Wherever an account is established for an ongoing transactional relationship, the best examples of these are wholesalers or suppliers.

When aren’t debit orders a good choice?

Okay, so when shouldn’t a debit order be your go-to solution? It seems every situation could warrant a debit order, but that’s not true. While there is no denying their value, this is when instead to give one a skip:

- Anytime a transaction needs immediate clearing, it’s wise to remember that debit orders are not instant and follow various timings. That said, there are many other ways to get paid immediately, such as through payment requests.

- If you want to purchase or deal in liquid assets or high-value goods like currencies, cars, and real estate, debit orders aren’t ideal because they are more attractive to fraudsters.

Debit orders with Netcash

Offering a simple and user-friendly interface, Netcash makes it easier to access and use debit orders for various payment types. With partnerships that seamlessly integrate into our payment solutions, your Netcash account is the key to unlocking the advantages of our accounting, payroll, and billing management.

How do debit orders work?

Before you or your business considers introducing a debit order management and collection solution, it’s time to get technical. As easy and straightforward as setting up a debit order might sound, there’s a lot going on behind the scenes.

In general, a debit order functions according to these four fundamental steps (with a detailed breakdown after that) :

- Authorisation: The initial step involves the account holder authorising the debit order agreement online. This is the debit order mandate, which specifies a payment amount and collection date.

- Bank Submission: Following the authorisation, the respective business submits a payment request to the account holder’s bank on the agreed date using an automated debit collections system and the Automated Clearing House (ACH).

- Funds Transfer: If sufficient funds are available in the customer’s account, the payment is processed and transferred to the business’s bank account. Keep in mind that if there aren’t enough funds available, the debit order will fail, but the system can (and will, in most cases) automatically attempt to process it the following day.

- Notifications: Finally, both the customer and business will be notified whether the transaction was a success or not. If unsuccessful, this notification is immediate, allowing any issues on either side to be dealt with promptly.

Though brief, the above does put the workings of a debit order into a short introduction. There’s still more you need to know, and it all begins with a mandate.

Debit Order Mandates

By now, the term ‘debit order mandate’ has been passed around quite a bit, and as most debit-order-related points go, while simple at the surface level, there’s more to it than meets the eye.

What is a Debit Order Mandate?

Think of a mandate as the legal and formal authorisation a customer gives to a business or service provider. This allows the indicated business or provider to automatically deduct a specified amount of money, at regular intervals, from the customer’s bank account.

How does a debit order mandate work?

The concept behind a debit order mandate is straightforward, and its reasoning rests firmly on convenience, efficacy, and security. That said, a successful mandate is the result of three key components:

- Consent: The mandate's consent requirement is an integral part of it. The customer needs to explicitly provide consent, either in writing, electronic consent, or verbally over the phone, to a company agreeing to initiate the debit order.

- Bank details: Alongside the consent, the customer must provide their bank account details, such as account number, branch code, and other bank-specific information.

- Authorisation: The third element of a successful mandate is authorisation. The customer is provided with the terms of the mandate, including the amount, the date or frequency of the payment, and any penalties for failed payments.

The mandate is binding and active once all the above are present, accurate, and verified.

What is the difference between debit orders and DebiCheck?

Aren’t debit orders and DebiCheck the same thing? The easy answer is no. While both require a mandate and amount to the authorised transfer of funds from the debtor to the creditor, DebiCheck is a relatively new kid on the playground and does things a bit differently.

Key differences you should be aware of are:

- A standard debit order or electronic funds transfer (EFT) debit order does not require immediate input from the bank in question. A DebiCheck debit order requires the customer to confirm the debit order with their bank via their banking app or online banking, and then the bank goes through a customer verification process.

- DebiChecks are far more secure because they require real-time customer verification and mandate authorisation. Standard debit orders demand manual verification and have historically been easy targets for fraudsters.

- With a standard debit order, banks only process it after the service provider submits it without verifying its legitimacy. Customers have to manually lodge disputes in cases like this. DebiCheck involves the bank immediately in authorising and confirming the debit order mandate.

DebiCheck and e-Mandates

Beyond the fundamental differences, DebiCheck differs from standard debit orders in that everything happens digitally. It removes the need for paperwork and manual intervention, which can cause issues down the line.

DebiCheck functions entirely electronically, from point A to Z, with much of the difference resting in its e-mandate functionality. This requires explicit confirmation from the bank account holder through DebiCheck. This is done digitally before any debit order can be processed.

This electronic mandate is considered binding once the customer agrees to the terms and conditions. Only then will deductions begin on the specified date.

Take the admin out of your collections

Chat to us about the best options for your business, or register for your account today.

How to use Netcash’s DebiCheck service for your business

Trusting Netcash with your debit order payments solution gives you full access to DebiCheck and its extensive range of functional and safety benefits. Being able to drastically reduce your risk of debit order disputes or complaints to your business, DebiCheck also increases the trust customers’ develop in your business.

Taking payments by debit order

While much has been said about debit orders' functionality and influence on the financial world, what does payment collection via debit order look like? Beyond the typical process a bank account holder should expect, what should businesses expect?

Well, let’s find out.

Mandate authorised collection

To kick things off, mandate authorised payment collections. This is the gold standard of formal agreements, indicating the amount, frequency, and payment terms. It does involve some steps, so let’s go through them.

1. Obtaining customer consent: This is the general first step where your customer is sent a mandate to accept giving their explicit authorisation. There are several ways this can be done:

- Paper-based mandates (traditional written consent)

- E-mandate (either online or electronic authorisation that is verified digitally)

- DebiCheck mandate

Note: A mandate requires the following details:

- The customer’s bank account details

- The agreed-upon amount (which can be fixed or variable)

- The date and frequency of the deduction

- The duration of the agreement

2. Submitting the mandate: After the mandate is obtained, it is submitted to either your payment collection provider, like Netcash, or your bank. During this step, the terms are set up for the automatic debit from the customer’s bank account according to the set schedule.

Batch payments

In contrast to collecting singular payments from customers, most businesses process batch payments, and there’s a lot of genius to it. Batch payments are an incredibly efficient way for businesses to collect multiple payments from hundreds of customers simultaneously, reducing administrative effort and cost. Here’s what the process looks like.

- Payment batch preparation: This involves gathering all the authorised debit orders for a specific period, whether daily, weekly, or monthly. Generally, this batch file would include all the relevant customer information, such as account details, amounts, and dates.

- Payment batch submission: Following the batch file preparation, it is submitted to the business's Payment Service Provider (PSP) or their bank. Think of the PSP as an intermediary between the company and the bank to facilitate payment collections. These PSPs are attractive solutions for businesses, especially with general automated reconciliation features.

- Payment processing: Next, the PSP or respective bank processes the batch on the agreed date (often called the action date). During this step, banks automatically debit the customers’ accounts, transferring the funds into the business’s account.

- Payment reconciliation: Finally, the business will receive a reconciliation report from their PSP or bank detailing which payments were successful or not. Failed payments can occur for various reasons, and companies may attempt a re-debit depending on the mandate's terms and conditions.

Taking debit order payments with Netcash

Whether you're looking to process batch debit order payments, Netcash offers your business an unparalleled level of fund management. Our innovative payment services manage your cash flow while providing your business with the ease of mind that comes from having a robust and reliable collections solution.

Debit Order Authorisation Process

A crucial element of a successful debit order is the authorisation process, and it takes on different angles based on whether you’re an individual or a business. Acting as the mechanism through which a company obtains permission from an individual to debit their bank account regularly.

The business’ guide to the debit order authorisation process

Businesses looking to collect payments via debit orders must follow specific steps to ensure they have the proper authorisation to debit a person’s bank account.

- Obtaining customer mandates: The initial step for businesses is obtaining customer mandates. These mandates could be an electronic authorisation request, DebiCheck authentication details, or DebiCheck authentication through their PSP account.

- Submission of authentication request (DebiCheck only): Businesses that use DebiCheck will then submit an authentication request to the respective customer’s bank, either in real-time (response times between 120 seconds and one day) or as part of a batch grouping.

Sidenote on mandate storing: Following the collection of the mandate, businesses must retain copies of it (either physically or electronically). Companies can refer to their mandate archive for any needed information on a dispute.

- Customer agreement: Once the customer agrees to the mandate terms and conditions and the authentication process is successful, the business receives full debit order authorisation.

Once the customer agrees to the provided mandate, the business and the respective bank can set up the debit order.

The individual’s guide to the debit order authorisation process

From the customer's perspective, the debit order authorisation process is more centred on providing consent than requesting it and generally follows a few steps.

- Understanding and agreeing to a debit order: You must fully understand the terms and conditions of the provided mandate as a customer before authorising any debit orders. Move ahead only after ensuring that you agree to the entire mandate.

- Mandate authorisation: After reading through the mandate, the next step is to provide the relevant bank account details, followed by the signature of the mandate. Keep in mind that mandates can take various forms, such as:

- Paper-based mandates

- Voice mandates

- Electronic mandates (E-mandates)

- DebiCheck mandates

- DebiCheck mandate confirmation: Remember that customers provided with DebiCheck mandates must actively confirm the mandate with their bank. These are the steps to follow:

- Customers initially receive a real-time notification from their bank of the pending mandate via SMS, mobile app, or email.

- This notification will prompt them to log in to their online banking platform or banking app or to visit an ATM to approve the mandate.

- Customers must verify the mandate details, including the amount, action date, and frequency, and confirm their consent.

- After the confirmation, banks will allow businesses to debit customers' accounts based on the agreed terms.

Once the mandate has been verified and authorised, the customers’ accounts will be debited on the specified date for a specific amount (fixed or variable) until the debit order is no longer valid.

Benefits of using Netcash for your debit orders

With extensive expertise in debit orders, partnering up with Netcash is the ideal solution for businesses looking to take advantage of our range of perks. With Netcash, you’re guaranteed:

- Flexible collection services that come with various solutions to suit your unique collection’s needs, from recurring and once-off debit orders to bank accounts and credit cards.

- Our eMandate solutions ensure that you obtain your client's authority to debit their account in a compliant, secure, and convenient way.

- You'll get paid sooner, thanks to our enhanced processing solutions. These solutions ensure that you receive up to 90% of your collection value on the day debits are processed.

- Extensive debit order reporting enables you to easily track customer accounts and analyse your debit order collections with comprehensive reports and statistics.

- Effective unpaid debit order management through our automated Payment Request sent via email/sms/WhatsApp message with a payment link, allowing your customers to pay via the Netcash Payment Gateway.

- Effortless integration with the top accounting, payroll, and business management software, allowing for process automation and avoiding of manual capturing and submission.

Streamline the collection of debit orders from your clients

Chat to us about your Debit Order needs or apply for your account now.

Debit Order Authorisation Process

A crucial element of a successful debit order is the authorisation process, and it takes on different angles based on whether you’re an individual or a business. Acting as the mechanism through which a company obtains permission from an individual to debit their bank account regularly.

The business’ guide to the debit order authorisation process

Businesses looking to collect payments via debit orders must follow specific steps to ensure they have the proper authorisation to debit a person’s bank account.

- Obtaining customer mandates: The initial step for businesses is obtaining customer mandates. These mandates could be an electronic authorisation request, DebiCheck authentication details, or DebiCheck authentication through their PSP account.

- Submission of authentication request (DebiCheck only): Businesses that use DebiCheck will then submit an authentication request to the respective customer’s bank, either in real-time (response times between 120 seconds and one day) or as part of a batch grouping.

Sidenote on mandate storing: Following the collection of the mandate, businesses must retain copies of it (either physically or electronically). Companies can refer to their mandate archive for any needed information on a dispute.

- Customer agreement: Once the customer agrees to the mandate terms and conditions and the authentication process is successful, the business receives full debit order authorisation.

Once the customer agrees to the provided mandate, the business and the respective bank can set up the debit order.

The individual’s guide to the debit order authorisation process

From the customer's perspective, the debit order authorisation process is more centred on providing consent than requesting it and generally follows a few steps.

- Understanding and agreeing to a debit order: You must fully understand the terms and conditions of the provided mandate as a customer before authorising any debit orders. Move ahead only after ensuring that you agree to the entire mandate.

- Mandate authorisation: After reading through the mandate, the next step is to provide the relevant bank account details, followed by the signature of the mandate. Keep in mind that mandates can take various forms, such as:

- Paper-based mandates

- Voice mandates

- Electronic mandates (E-mandates)

- DebiCheck mandates

- DebiCheck mandate confirmation: Remember that customers provided with DebiCheck mandates must actively confirm the mandate with their bank. These are the steps to follow:

- Customers initially receive a real-time notification from their bank of the pending mandate via SMS, mobile app, or email.

- This notification will prompt them to log in to their online banking platform or banking app or to visit an ATM to approve the mandate.

- Customers must verify the mandate details, including the amount, action date, and frequency, and confirm their consent.

- After the confirmation, banks will allow businesses to debit customers' accounts based on the agreed terms.

Once the mandate has been verified and authorised, the customers’ accounts will be debited on the specified date for a specific amount (fixed or variable) until the debit order is no longer valid.

Benefits of using Netcash for your debit orders

With extensive expertise in debit orders, partnering up with Netcash is the ideal solution for businesses looking to take advantage of our range of perks. With Netcash, you’re guaranteed:

- Flexible collection services that come with various solutions to suit your unique collection’s needs, from recurring and once-off debit orders to bank accounts and credit cards.

- Our eMandate solutions ensure that you obtain your client's authority to debit their account in a compliant, secure, and convenient way.

- You'll get paid sooner, thanks to our enhanced processing solutions. These solutions ensure that you receive up to 90% of your collection value on the day debits are processed.

- Extensive debit order reporting enables you to easily track customer accounts and analyse your debit order collections with comprehensive reports and statistics.

- Effective unpaid debit order management through our automated Payment Request sent via email/sms/WhatsApp message with a payment link, allowing your customers to pay via the Netcash Payment Gateway.

- Effortless integration with the top accounting, payroll, and business management software, allowing for process automation and avoiding of manual capturing and submission.

Debit order timings

Another essential element businesses and customers must remember is debit order timings. Understanding these timings is critical for companies to ensure a smooth payment processing system and manage their cash flow.

Let’s look at the fundamental concepts involved with debit order timings, starting with pre-payment timings:

- The action date: Think of the action date, or processing date, as the specific day banks process debit orders. On this day, banks will debit customer’s accounts for the agreed-upon amount. Generally, businesses will set up debit orders on fixed dates, such as the 1st, 15th, 25th, or the last business day.

- Submission deadlines: While businesses prefer to batch their debit order payment collections, banks typically rely on processing debit orders using batch systems. This means companies must submit their debit order instructions to their Payment Service Provider (PSP) or bank at least one to two days before the intended action date.

What happens if businesses miss the submission cutoff for debit orders? Well, in these cases, they can submit the batch the following day for processing on a later action date. Alternatively, they can re-run the debit order on another day, which is necessary if payments fail due to insufficient funds.

Next up, here’s what you should know about timings after payment submission

- Clearance and settlement: Once debit orders have been processed on their respective action dates, funds normally take one to two business days to clear and settle into the business’ bank account.

How long do debit order mandates last?

Authorisation? Check. Process? Check. Duration? Coming right up. An important aspect is precisely how long a debit order mandate lasts. Well, let’s do a quick breakdown:

- Standard mandates: These generally remain in effect until the specified period as per the agreement ends. This includes subscription billing, loans, and insurance payments.

- DebiCheck mandates: Requiring more formal confirmation from the customer, DebiCheck mandates are valid for the duration to which both parties agree. These are usually the most valuable for service contracts and will expire once the service term ends.

- Mandate expiry: Debit order mandates can expire if not used within a certain period, generally between three and six months. Banks may automatically expire the mandate after such a period and could require a new mandate to be set up for future debits.

Streamline the collection of debit orders from your clients

Chat to us about your Debit Order needs or apply for your account now.

Creating and managing debit orders for payment

Beyond the creation of batch and individual payments, there is a surge in digital adaptation in debit orders. Gone are the days when debit order payments had to be done manually. Although it is still an in-use practice, the need for digitisation has made it easier than ever to integrate technological advancements into the debit order collection process.

Software integrations

More and more South African businesses are turning to innovative tech and software integrations through leading Payment Service Providers (PSPs) or other financial institutions to handle their debit order system more efficiently.

Alongside these PSPs' various attractive features, their role as intermediaries extends into collecting, processing, and reconciling debit order payments. Each provider offers a collection of API-based software integrations that seamlessly integrate the business’ existing systems, such as CRM, ERP, and other accounting software.

These API integrations have various functionalities, ideally automating debit order setups, payments, mandate management, and payment reconciliation. In addition to these critical features, these integrations could enable automated mandate creation, real-time payment status tracking, and secured processing.

Do these integrations cover batch payment processing? Of course, they do. They make it even easier and more efficient for businesses to upload batch files and automate scheduling, which reduces administrative costs and hours.

Beyond these future-focused software solutions, remember that various debit order collection systems are already integrated daily into solutions such as Sage and Xero. Other integrations aim to improve debit order security and compliance, ensuring relevant PCI-DSS and PASA compliance.

How to manage/use debit order reports

An essential aspect of debit order systems is their transparency. While previously, there were dozens of potential grey areas, these days, debit order reports have elevated how much of an overview businesses have across their debit orders.

Debit order reports provide crucial information on various elements, including transaction statuses, mandate authorisation, failed payments, and batch processing.

Looking a bit deeper, debit order reports allow for far more accurate payment performance tracking, which businesses can use to accomplish a variety of tasks, such as:

- The monitoring of debit order success rates.

- Identifying potential trends in customer payments.

- Predicting which customers may need additional payment reminders.

Debit order reports also contain vital information regarding reconciliation and accounting. These reconciliation reports are pivotal in aligning customer payments with financial records. This, in turn, enables automatic reconciliation in accounting systems.

A typical debit order report makes it easier for businesses to evaluate failed payments and decide whether or not to re-run specific debit orders. Another advantage of these reports is their predictive element, which helps companies identify future payment issues.

Using this data, businesses enhance their communication capabilities, allowing them to send payment reminders, failed payment notifications, payment requests, and payment success confirmations.

Finally, businesses can utilise debit order reports to reduce unpaid debit orders. Taking advantage of PSP dashboards, these reports allow for the dissection of unpaids and the reasoning behind them. Typically, these are represented as codes that expand payment statuses, which furthers the enhanced communication should an issue arise that needs fixing.

A quick breakdown of debit order codes

Highlighted within debit order reports, you’ll quickly notice codes corresponding to specific transaction results. Knowing these codes helps businesses understand why payments succeeded or failed. You can browse through this report for examples of unpaid codes and what they mean.

Rules for resubmission of debit orders

Should a debit order fail, businesses can often resubmit it; however, there are specific rules and guidelines that they must follow. PASA outlines these as:

- Resubmission timing: When a debit order fails due to insufficient funds, it can be resubmitted, but businesses must adhere to a specific timeframe. The timeframe typically allows for resubmission within seven days of the original action date.

- DebiCheck resubmissions: If the initial debit order fails due to the customer not confirming the mandate, businesses can notify the customer to approve it again. After getting permission, the debit order can be resubmitted.

- Resubmission reasoning: A debit order should only be resubmitted if the reason behind the failure is resolvable, such as insufficient funds, account closure, or incorrect details.

- Customer notification and consent: Businesses must inform customers when resubmitting a debit order, especially for recurring payments. Remember that the customer must agree to the resubmission.

- Maximum resubmission attempts: Businesses are usually allowed to attempt resubmission once or twice after the initial debit order fails. However, this can change depending on the PSP or bank’s policy.

How to collect unpaid debit orders

Businesses are, unfortunately, not immune from unpaid debit orders. Luckily, there are various ways to effectively collect these payments after the initial failure. Options available to businesses include:

- Resubmission of the debit order, typically within seven days.

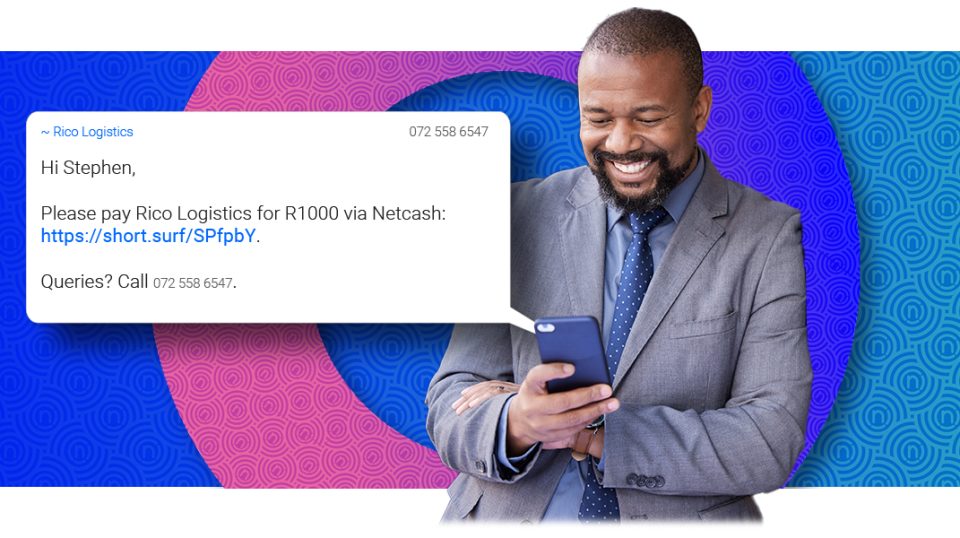

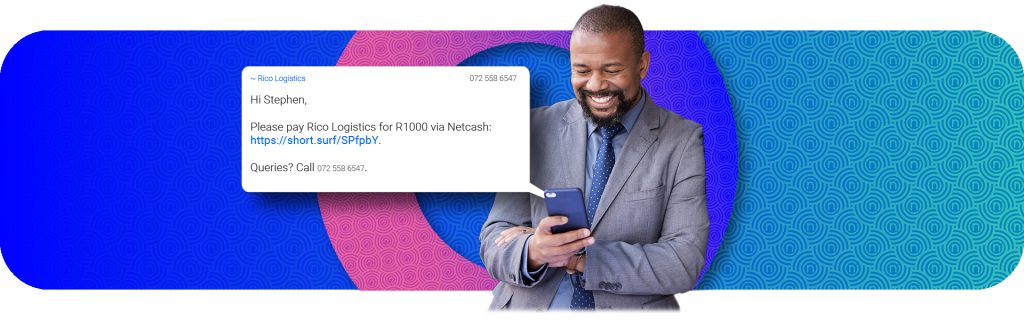

- Direct customer communication through payment requests that can be sent via email or SMS, WhatsApp messages, and QR codes. These requests direct customers to a secure online link to complete the transaction.

- The business can re-run the debit order after getting customer consent.

- Businesses can offer alternative payment methods such as Instant EFT, credit card payments, or online payment gateways.

- For customers with financial difficulties, the best solution is to negotiate a payment plan, which could include instalment plans.

- Specific penalty fees could be charged if applicable and communicated within the debit order mandate.

- Automated PSP features should include the automation of debit order retries, as well as reminders for unpaid debits.

- As a last effort, businesses can resort to debt collection or legal action, which is more suited to collecting larger debts.

Transferring debit order mandates

Okay, by now, we’ve surely covered everything debit order mandate-related, right? Let’s dive into the final chapter of debit order mandates – transferring a debit order mandate. To best explain everything you need to know, think of something as casual as a gym membership.

For the duration of the membership, up until the present day, the gym in question has been happily and successfully debiting customer accounts every month. Now, the gym has decided to switch payment providers and must transfer their existing mandates.

What does this process look like?

First, the gym must notify all its customers about the planned switch, which should be done well beforehand. Then, the gym will send out a consent request, asking for explicit consent to transfer the mandate to their new provider. After being given the green light, the debit order mandate is securely transferred. The best bit? Payments continue uninterrupted.

The legal side of transferring debit order mandates

Behind the scenes, PASA (the Payments Association of South Africa) has set aside specific legal frameworks for transferring a debit order mandate. At its core, PASA has regulations that say the gym needs your explicit permission before transferring the mandate. Without it, the transfer is a no-go.

Why a business may change payment providers

While a business might change payment providers for many reasons, they generally do so to cut costs, improve debit order collection efficiency, or use a more secure system. Think of it as a business's way of adapting its systems behind the scenes so things run more smoothly.

Choosing a Debit Order Provider for Your Business

Let’s look at why a business would choose to use a PSP for debit order collections in the first place. It’s important to know companies turn to a payment service provider to make their operations easier, removing unnecessary complications. These are some considerations businesses face:

- Fee structure: One of the most vital things to evaluate is the relevant PSP's fee structure, which should highlight transaction fees, setup fees, and hidden fees.

- Security: Next up is debit order safety. Top-notch PSPs recognise the need for improved security and should offer data encryption alongside PCI compliance.

- User experience: Consider elements that might hinder rather than help to ensure that the payment process is as smooth as possible. For example, consider easy integration into existing systems and a user-friendly interface.

- Payment options: Another critical element to focus on is whether or not the relevant PSP offers options. These can range from credit card payments to mobile and online payments.

- Customer support: When something goes wrong, the ideal PSP should have a solid customer support system and team that can assist you 24/7 across various channels.

- Scalability: Partnering up with a PSP that can grow alongside your business is beyond crucial, so keep an eye out for a PSP that can handle increased transaction volumes.

Why choose Netcash?

Netcash is the perfect choice for your business. With our industry-leading solutions, you’re one step away from streamlining your recurring payments. Optimising your cash flow through our revolutionary collections services, we’ll manage your entire debit order process, offering flexible collections options, eMandates, and payment reporting.

Our seamless integration capabilities allow for effortless adaptation into your existing systems, ensuring your payment processes are smoother and more efficient. Our simpler and user-friendly interface makes it easy to access and use debit orders for various payment types. Your Netcash account is the gateway to enhanced financial control and management.

Debit order compliance in South Africa

Alongside the various fundamentals of debit order collection, businesses have to navigate a landscape of compliance rules and regulations. Only after each is sufficiently met can a company be fully compliant and authorised to debit.

Rules and regulations

The Payment Association of South Africa (PASA) and the National Credit Regulator (NCR) are the top authorities on debit order issues, and both have established rules to ensure the smooth and legal operation of debit order systems.

These include regulations that pertain to:

- Mandate requirements

- DebiCheck criteria and requirements

- Transparency

- Timely notifications

- Data protection (in adherence to the Protection of Personal Information Act, or POPIA)

- The handling of failed payments

- Required documentation for each debit order

What it means for your business

Rules and regulations accounted for, what exactly do they mean for businesses? Most importantly, adhering to these frameworks ensures that companies avoid fines, penalties, or legal issues.

Beyond avoiding negative consequences, businesses that meet these regulations build trust with customers and other companies. After all, nobody wants to do business with a company that sidesteps the rules.

In addition to the above, businesses that remain on the right side of these rules benefit from streamlined processes, which make debit order collections easier. This also improves their payment management in accordance with all regulatory bodies.

Managing your risk with Netcash

As a valuable resource for business, Netcash offers extensive, thorough, and compliant risk reports that are vital to assessing whether your business might be at risk. This allows you to quickly verify new employees, clients, or suppliers, which reduces financial and security concerns. Our risk reports source data from The Companies and Intellectual Property Commission (CIPC) and multiple credit bureaus, giving you more accurate information.

Ready to expand your reach with voucher payments?

Discover how Netcash helps you serve unbanked communities with secure, flexible payment options.

Author:

Paul Adant

Business Solutions Manager

Stay in Touch![]()

![]()

![]()

![]()

Paul Adant has over 30 years experience in banking and the payment industry, he has a passion for translating needs into effective solutions. Cultivating strategic partnerships with integrated software vendors and producing cost effective, efficient and time saving business solutions make him a valuable member of the team at Netcash.

{kind=link}

{kind=link}

{kind=link}