Get ahead of the ins and outs of successful gym management (2024)

April 8, 2024

Digital payment services in South Africa: Methods, trends & more

May 16, 2024Customers are increasingly looking for convenient and secure ways to make payments online, and digital payments processing plays an integral role in this. Business owners aware of this demand are scrambling to integrate digital payments into their operations. Are you among them?

GIVE CUSTOMERS THE PAYMENT OPTIONS THEY WANT TO SEE

It is clear that the digital payments landscape is changing. The rise of mobile payments and the integration of omnichannel experiences supports this. As a business owner, you want to keep abreast of these evolving trends, especially since the South African eCommerce market is expected to be worth over R400 billion by 2025.

Naturally, you may wonder what digital payments are and how online payment processing works. Perhaps you’re looking to discover the different ways of processing payments online. Either way, you’ve come to the right place. This comprehensive guide will help you figure out all you need to know about digital payments processing when selling online, including information on payment gateways and processors.

What is a digital payment?

So, what is a digital payment? These are payments made via digital or online means. When making online payments, no exchange of cash occurs.

Digital payments are also referred to as electronic payments. The payer (person making the payment) transfers money from their payment account to the payee’s (the person receiving the transfer) account.

For your customers to make payments online, you need a payment gateway. This technology facilitates secure online transactions, so your virtual cash register rings with each successful sale.

Payment gateways

Payment gateways allow you to seamlessly and securely process online transactions. Think of them as intermediaries that act as a bridge between your customers’ payment information and your merchant account. This piece of technology encrypts sensitive information, like credit card details your customers type in, to protect them from potential threats online.

As you can imagine, your customers entering their credit (or debit card) information, like card numbers, expiry dates, and CVV (card verification value) numbers, is them trusting their sensitive financial information with you. Using a secure and reputable payment gateway will help encrypt their data and securely transmit it to their accounts for authorisation.

When they approve the transaction, the funds will be transferred from their account to your merchant account. And there you have it; the transaction will be complete.

OFFER MULTIPLE PAYMENT OPTIONS TODAY

Payment gateways don’t just offer your customers security in online payments processing — they also streamline the checkout process, making it super quick and easy for them to shop online. This payment technology accepts a variety of online payment processing methods. From buy now, pay later to digital wallets, online shoppers are spoilt for choice.

In addition, you can easily and securely accept payment from your customers, be it via a website or mobile app. One could say that payment gateways revolutionised eCommerce. Without them, businesses and customers wouldn’t enjoy the unrivalled ease and security they do today.

Payment processors and payment processing explained

Up till now, you’ve gotten a bit of an understanding of payment gateways and the important role they play in digital payments processing. You’ll uncover more information on payment processors and how payments processing works as you continue reading.

What is a payment processor?

A payment processor is a company that facilitates online transactions by acting as a mediator between both the customer’s and the business’s banks. It helps transfer funds securely and accurately.

How the online payment process works

When your customer clicks “checkout,” what follows is a series of events that ensure a smooth and secure online transaction. Below, you’ll find a simplified breakdown of the process. Online or web payment processing works in the following way:

- Your customer clicks “checkout” to clear their cart: This is when they choose any of the available payment options, be it credit/debit card or Instant EFT. Then, they enter their payment details, which typically include their card number, cardholder name, card expiry date, and CVV (card verification value) number.

- The payment gateway authorises the transaction: After checking out and entering their payment details, the payment gateway acts as a secure intermediary. It encrypts the sensitive information your customer has entered and sends it to the payments processor.

- The payments processor verifies the information: Once the payments processor receives the customer information, it then verifies these details with the customer’s bank. This bank is also referred to as an “issuing bank,” which is the financial institution that issued the card to the customer.

- Success! Transaction approved: When the payments processor has successfully verified the customer’s information, the issuing bank approves the transaction and authorises the transfer of funds to the merchant’s account.

- Transfer of funds to the merchant’s account: The payments processor sends details of the authorisation to the merchant’s bank. Also known as the “acquiring bank,” it then transfers these authorised funds to the merchant’s account.

- The customer is notified of the transaction being successful: Finally, the merchant is notified of the transaction being successful and sends the customer a confirmation.

Who is involved in electronic payment processing?

As mentioned earlier, a payer makes the online payment to the payee. But these aren’t the only participants. Below, you’ll find the different parties involved in the process.

Payer/Customer

The payer is the customer. This is the person paying for the goods or services you sell. Let’s say you run a small accounting firm. An example would be a business paying you for accounting and payroll services.

Payee/Business

The payee is the business (i.e., your company) receiving funds from the customer in exchange for goods or services. Following the example above, your organisation (i.e., the small accounting firm) would be the payee.

Payment gateway

Payment gateways facilitate online transactions by transmitting payment information between the web portal and the bank. If you had an online store with Netcash Shop for your small business, it would have Netcash’s eCommerce payment gateway automatically installed, and this would process your customers’ transactions from your website to your merchant account..

CATER TO MORE PAYMENT PREFERENCES

Payment processor

While a payment processor and gateway may sound similar to some, they serve different functions. Once the payment gateway passes the payment details, the payment processor enters the picture.

True to its name, it processes the transaction. This involves technical aspects, such as verifying the payment details, checking if there are sufficient funds, and communicating with the customer’s and merchant’s accounts.

All of this happens in no time, within seconds. A payment processor essentially completes the online transaction the payment gateway initiated.

For example, when your customer pays you for accounting services, the payment processor could be, for example, PayGate

Device

To make the payment, the customer will need a device. This could be their smartphone in the case of paying via their digital wallet, or it could be a laptop they use to make payments online.

The payer’s/customer’s bank account

Since funds will be transferred from your customer’s account, their bank (that issued them their debit or credit card) is also a participant. If your customer banks with First National Bank for example, then their FNB bank account would be involved in the process.

The payee’s/business’s merchant account

Likewise, your merchant account is involved in the process, as this is the account to which funds will be transferred from the customer’s account. Following the example above, if you had a merchant account with Standard Bank, that account would be a participant, or if you were a Netcash Payment Gateway client, you’d have a Netcash merchant account

The payer’s/customer’s payment scheme/network

This is the payment network (e.g., Visa) that is linked to the payee’s/customer’s card. The payment network links the payment processor and the payee’s/customer’s bank. If your customer’s card has the Mastercard or Visa logo, that would indicate which payment network is involved.

Merchant accounts

For your business to receive and collect online payments, you need a merchant account. This business bank account allows you to accept electronic payments from customers. Major banks like Standard Bank, First National Bank, ABSA, and Nedbank, to name a few, offer merchant accounts. Most payment gateways will also create a merchant account for you, and funds received from transactions via the gateway will all be securely deposited into this account.

Security

Online transactions involve a lot of sensitive financial information. Think CVV (card verification values) and card numbers, customer names, and residential addresses. As such, ensuring that digital payments are secure is paramount.

The intermediaries that facilitate online payments, payment processors, play an important role in this regard. They help prevent fraudulent activities, securing customer data in the process.

OFFER FLEXIBLE PAYMENT SOLUTIONS

The importance of security in online payment processing

From keeping customer data secure to regulatory compliance, here are several reasons digital payments need to be secure:

- Protects customer data: If there’s a security breach within your payment processing system, your customer’s information could be exposed. This may lead to sensitive customer data like credit card details landing in the hands of cybercriminals. The result? Identity theft, financial losses, and possibly losing your customers’ trust.

- Safeguard the reputation of your business: If your organisation experiences a data breach, which leads to your customers being defrauded, your company could lose money due to lawsuits, lose customers, and make less revenue. Should news of this get out, your business may gain a negative perception.

- Regulatory compliance: The payments industry has strict standards, requiring payment processors to adhere to them. Examples include the Payment Card Industry Data Security Standard (PCI DSS), which helps protect customer data. Netcash is a secure online payment gateway and is PCI DSS Level 1 Compliant, the highest level of compliance in the industry, so you can rest assured your customer’s payment data is safe and secure.

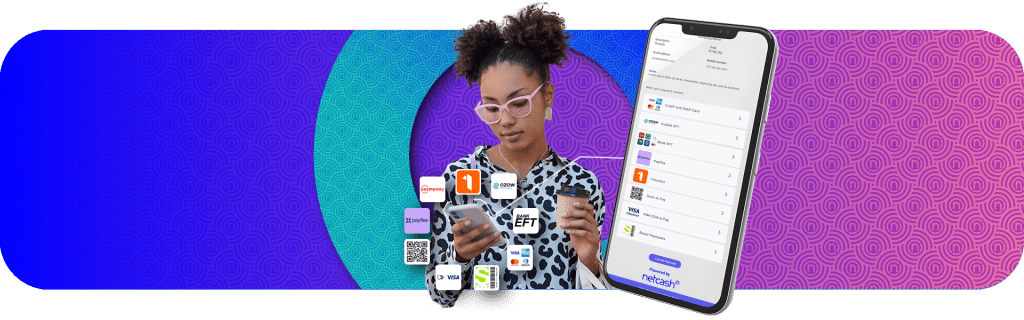

Online payment processing methods

Different methods of online payments exist, but before you can offer these to your customers to make paying easier for them, it’s important to understand what they entail. The below will touch on them briefly and also explain their pros and cons.

Credit/debit card

Credit and debit card payments are the most widely used digital payment methods due to the convenience and security they offer merchants and customers alike. In addition, these help both parties avoid the hassle of carrying cash and the security risks of handling cash.

Pros

- Customers are most familiar with paying with a debit or credit card.

- Credit and debit cards can offer protection against fraudulent transactions.

- Helps businesses glean valuable customer insights.

- Credit and debit cards are widely accepted across the world.

Cons

- More expensive to process online payments for credit and debit cards.

- Also has a higher risk of chargebacks if customers dispute transactions.

SA examples/brands

Examples of this within the South African context include Mastercard and Visa. Statistics show that 51% of South African card holders had Visa cards in 2022. Mastercard trailed slightly behind at 47%.

Scan-to-pay (QR)

This type of online payment includes the use of QR (quick response) codes when making mobile payments. Customers can use their smartphones and scan to pay with a QR code.

ADD POPULAR PAYMENT METHODS TO YOUR CHECKOUT

When your customer scans the barcode with their phone at checkout, they will be able to instantly transfer money from their mobile wallet or linked bank account. This mobile payment solution is the next stage in the evolution of mobile payments.

Pros

- Scan-to-pay is simple and user-friendly.

- Helps eliminate the need for customers to carry cards or cash.

- Merchants also find them to be cost-effective.

- Compatible with different mobile platforms.

- Can reduce customers’ exposure to card skimming.

Cons

- Compared to credit and debit cards, these aren’t as widely accepted.

- Paying via QR codes may not be suitable for high-value transactions, such as paying for a house deposit or buying a car.

SA examples/brands

SnapScan, Masterpass™, and Zapper™ are examples of the scan-to-pay payment service. Many retailers like Shoprite accept QR code payments.

Tip: With Netcash, you can provide your customers with a single QR code which they can then use to choose almost any digital wallet app to pay with.

Digital wallet

Digital wallets, with certain banks and brands like Apple and Google, help securely store customers’ payment information, which they will then use for payment at a later stage.

Pros

- Feature enhanced security and offer convenience to users.

- Digital wallets streamline the checkout process.

- Allow for peer-to-peer transfers

- Customers enjoy in-app purchases.

Cons

- Customers will have to set up and manage their digital wallets.

- Not all merchants accept customers paying online in this way.

SA examples/brands

Digital wallets available to South Africans include Google Pay, Apple Pay, and Samsung Pay. Other wallets used in the country are Fitbit Pay and Garmin Pay.

Contactless payments

With a user’s credit or debit card information securely stored on their device (i.e., smartphone or smartwatch), contactless payment methods such as Apple Pay and Google Pay allow customers to pay transactions with their mobile device. All it takes is the wave of their phone, and that’s it. Payment made.

Another way customers can make contactless payments is simply holding their credit or debit card close to a speed point and paying. Also known as “tap and go,” contactless cards contain RFID (radio frequency identification) chips in them.

ACCEPT ALL MAJOR PAYMENT METHODS NOW

Pros

- Contactless payments are fast and convenient when paying for in-store transactions.

- With their tap-and-pay technology, they offer customers enhanced security.

- Are more hygienic as they limit contact with point-of-sale devices.

- Offering contactless payments can help businesses increase sales, as it makes paying a hassle-free experience for customers.

- Businesses may replace point-of-sale devices and speed points less often due to less wear and tear from reduced physical contact.

Cons

- These require point-of-sale (POS) terminals that are compatible. This may be quite costly for business owners.

- Contactless payments may not require a PIN for transactions below a certain amount. This exposes their owners to the risk of fraudulent transactions made with their cards if lost or stolen.

SA examples/brands

Banks that allow for contactless payments in South Africa include First National Bank, ABSA, and Standard Bank. It is estimated that contactless payments account for over 50% of digital transactions in the country.

Buy now, pay later

With buy now, pay later services (BNPL) such as PayJustNow, Payflex, Happy Pay, and more, customers have flexible options for online payments. These online payment services allow customers to pay for their purchases in instalments.

Buy now, pay later allows customers to make payments spread over four weeks to three months (or even longer). What draws many customers to making online purchases this way is that they aren’t charged interest.

Pros

- Due to flexible payment options, this can attract more customers and lead to higher sales.

- Customers may order more products per order, which can lead to increased average order values.

- Helps reduce upfront costs for customers, leading to improved customer satisfaction.

Cons

- By adding buy now, pay later as a payment option, some merchants may incur additional fees.

- This can increase a business’s risk of bad debt as customers may order more than they can pay, leading to defaults on payments.

SA examples/brands

Buy now, pay later brands in South Africa include Payflex, PayJustNow, Happy Pay, and Float. Payflex allows customers to pay over six weeks in fortnightly instalments. With Float, customers can pay over 24 months.

OFFER MULTIPLE PAYMENT OPTIONS ON YOUR ECOMMERCE WEBSITE

Instant EFT

This is a secure and cost-effective way for customers to make payments. With some online magic, Instant EFT directly transfers funds from the customer’s bank account to that of the merchant.

Pros

- Instant EFT allows for the secure, direct transfer of funds from one account to another.

- It is typically cost-effective for merchants and customers, ensuring a win-win situation.

- Processes transactions in real time.

Cons

- The customer will have to manually initiate the payment themselves.

- Instant EFTs may not be suitable for recurring payments like bank EFTs.

SA examples/brands

Paying via Instant EFT has gained popularity as a swift and secure way to pay. Prime examples of Instant EFT services in South Africa include Ozow and banks’ own services via online banking.

Bank EFT

Bank EFTs are also known as direct debits or direct deposits. This online payment method allows customers to authorise the deduction of recurring payments from their bank accounts.

Pros

- Bank EFTs are fast and convenient for recurring payments.

- Widely accepted by both merchants and customers.

- Compared to other payment methods, they also attract lower processing fees.

Cons

- May not be the best way to pay for impulse purchases.

- It also requires you to authorise online payments at your bank before using it.

SA examples/brands

Examples of South African companies and brands that offer bank EFTs include Standard Bank, ABSA, FNB, and more.

Secure and reliable digital payments processing with Netcash

With the rise of eCommerce and online transactions, it is important to master digital payments. No longer a nicety (or necessity, for that matter), integrating online payment solutions with your offering is a strategic move for your business.

Ready to make the move? Netcash is a reputable payment solutions provider with two decades of experience in the payments industry and can help you process digital payments with ease. Chat with Netcash to get started and discover how you can take your electronic payment process to the next level.

OFFER MULTIPLE PAYMENT OPTIONS ON YOUR ECOMMERCE WEBSITE

Author:

Brent Felix

Payment Advisor

Stay in Touch

![]()

![]()

![]()

![]()

Brent isn’t just a payments guy, he’s your payments ally. With a background in banking and experience navigating the world of payments, he’s passionate about connecting businesses with the right tools to scale and secure their online success. Charming and confident, Brent makes the complex world of e-commerce payments clear and conquerable. He’ll help you unlock the power of secure and scalable solutions, ensuring your business is ready to thrive online.

{kind=link}

{kind=link}

{kind=link}

{kind=link}