Netcash Partnerships Geared to Streamline Payment Processes

October 7, 2020

Biometric login on our mobile app

December 15, 2020Consumer adoption of QR code payments has accelerated during the pandemic, partly due to merchants and consumers looking for contactless ways to transact as opposed to cash or cards. Yet there are still many myths about the technology, with some small and mid-sized companies believing that adopting QR codes in their business will be complicated, expensive and insecure.

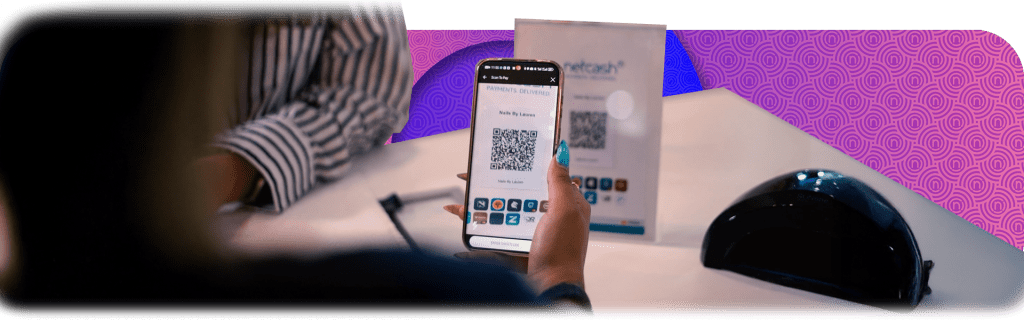

Before we debunk some of these myths about contactless payments, let’s take a step back and look at the technology. Short for Quick Response barcode, a QR code is a data-rich code that can be read by digital cameras, including those that come standard with most smartphones. It can contain a range of information, including a menu, a coupon, a URL, contact details, payment or billing information and much more.

QR codes have been in South Africa for a while, with fintech companies pioneering the technology as an instrument for making and accepting payments. To use a wallet, customers download an easy-to-use app from their smartphone app store and then add the details for their debit or credit cards. They can then scan the QR code and pay from their phone.

Today, it’s not just fintech innovators who offer QR codes for payments, but also credit card companies and most South African banks. QR code payments have become a standard feature in smartphone banking apps. Yet myths prevail about QR codes among consumers and small to medium sized businesses. Let’s look at why these perceptions may be outdated.

QR codes are a gimmick for early adopters or a new way for fintechs to make money

Many consumers and merchants still think of QR code payments acceptance as a flashy technology for early adopters. Yet QR codes are found nearly everywhere today – printed on bills from major utility companies, at the point of sale at major national supermarket chains, at checkout on e-commerce stores, and in parking lots at shopping malls.

QR codes streamline transactions by allowing people to scan to pay. This can speed up transactions in face-to-face settings like shops or the delivery of a service at a customer’s home. It can also help small businesses get paid faster when invoicing customers. If you put a QR code on your invoice, your customer can scan and pay without needing to log onto online banking or inputting card details in a third-party payment gateway.

The technology is complex

Many small companies think it will be difficult and expensive to implement a QR code payment solution. They imagine it will involve special payment terminals, complicated integrations with accounting and point of sale systems, or steep monthly fees and transaction costs. They are also concerned that they will need to support numerous digital wallets and apps.

The truth is there are solutions that offer low transaction costs without tying you into a contract. They allow you to generate QR codes and accept payments with nothing more than a standard iOS or Android smartphone. These solutions are also interoperable with most QR code wallets, which means your customers can pay with whichever wallet or banking app they prefer.

The risks of fraud and abuse are high

Some merchants and consumers are concerned that mobile and digital transactions are riskier than cards and cash. However, transacting via QR code is safer than using physical cards. Given that consumers are still effectively paying by card, even if they no longer need to present the plastic, the protections the card companies and banks offer consumers and merchants still apply. For example, illegal or fraudulent payments can still be disputed.

In addition, removing the physical card from the transaction reduces the consumer’s exposure to risks such as card skimming. Consumers will also generally need to authenticate any transactions with a fingerprint or PIN code. The built-in intelligence in some apps will add another layer of security by requesting a one-time PIN when payment patterns change (new merchants, different locations, etc.).

Supporting consumer choice

When it comes to QR code functionality, a robust payments solution will make it easy to display QR codes at pay points, quotes, invoices, statements or till slips and to generate a QR on a smartphone app. It should support multiple wallets and banking apps so customers don’t need to download yet another app to process a payment.

Integration with point of sale and accounting solutions will further streamline the payments environment. Netcash, for instance, reconciles payments easily with several leading accounting and ERP solutions. What’s more, each branch or till point can have its own QR code to track payment receipts at point of sale.

By making it more convenient for customers to pay means merchants can get paid faster and with less hassle. It also reduces the risk of losing a sale because the business doesn’t support the customer’s preferred payment method. Merchants should look for a payment solution that makes it easy to accept a wide selection of payments types, including bank and instant EFT, card, QR codes, cash and Visa Click to Pay.

– Percy Schultz | Sales Director at Netcash

About Netcash

Established in 2003, Netcash is a payment solutions provider delivering debit orders, salary and creditor payments, Pay Now, eCommerce, and risk report services to South African businesses and organisations. The company provides multiple innovative and integrated online payment solutions that are efficient, simple, and cost efficient. Netcash is registered with the FSCA, PASA and is PCI DSS Level 1 compliant.

{kind=link}

{kind=link}

{kind=link}

{kind=link}